Introduction

- 1700 – cases of insolvency in the construction industry nationwide on average every year

- 20-25% – of all insolvencies in Australia are in the construction industry

Where do these potential industry risks come from? Firstly, from property market conditions where work levels ebb and flow in line with demand. Secondly, from a culture of underbidding, which squeezes those both at the top and bottom of the chain, with contractors and subbies coming off worse.

On top of this, your building and construction businesses can suffer financial distress for more specific reasons. For example, you may have made a mistake in estimation, or have a contract that’s run out of money due to subcontractor delays.

The outcome? You go from a sure profit to a small profit to a loss. If you’re unable to meet this loss and improve your cash flow, you can become financially unstuck. From here, the prospect of insolvency grows brick by brick in front of you.

In this e-book, we take an in-depth look at the challenges construction companies face and offer our recommendations on how you can turn things around if your business is experiencing financial difficulties. We also cover the worst-case scenario – insolvency – looking at both your legal obligations and formal appointments.

Chapter 1:

Managing the risks

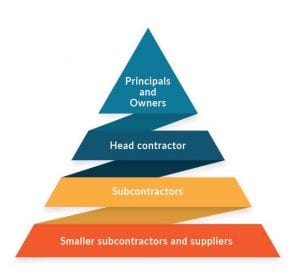

Understanding the construction pyramid

If you’re a subcontractor performing most of the work, you don’t have a direct contractual relationship with the principal for whom the works are being done and who is ultimately financing the project. This power imbalance means failures up the top cascade down, increasing your risk of insolvency.

Managing the risks

Getting your contract right can help ensure potential insolvency risks of companies either above or below you in the pyramid are sufficiently managed. It can also lessen your company’s liability where unexpected events affect a project.

Here are some things to cover:

- Clearly and correctly identify who each party is to the contract (for example, with their registered business entity and ABN).

- Outline the key roles and responsibilities for each party to the contract, and make sure they are enforceable obligations.

- Ensure that each party to the contract is only taking on risk that it controls and, where it does not control the risk, is properly able to obtain insurance to manage that risk.

- Establish ownership of materials brought to site and ensure those materials are not unlawfully removed.

- Have a clear programme with appropriate mechanisms for managing and, if necessary, extending time for delivery.

- Clarify the right to terminate or suspend work in the event of insolvency or suspected insolvency.

- In the event of termination, incorporate a clause enabling the retention of future contractual rights.

- Clearly identify what’s required for completion of the works, or practical completion, under the project and ensure those requirements can be met.

If you’re the principal of a construction project:

- Register an interest on the Personal Property Securities Register (PPSR) to gain priority in the event of insolvency.

- Obtain appropriate security and insurances from the contractor.

- Incorporate proof of payments to subcontractors and sub-subcontractors as a pre-condition for progress payments.

- Only allow for the payment of materials or goods not incorporated into the works in very limited circumstances, and in those circumstances, ensure there’s a PPSR registration.

- Where appropriate, include provisions to allow an audit of the contractor to ensure that payments are being made.

- Have clear rights of suspension and termination in the event of non-performance by a contractor.

- Demand the novation of subcontractors to enable you to step into the shoes of the insolvent contractor and have its subcontractors complete their works.

If you’re a head contractor:

- Obtain appropriate security and insurances from subcontractors and suppliers.

- Ensure that the risks taken under the head contract, including any design requirements or obligations around completion, can be met and properly managed.

- Take advantage of your right to suspend work under the contract for non-payment.

- Include clauses in your contracts to protect ownership of materials and equipment.

- Register security interests on the PPSR so they are enforceable in the case of insolvency.

- Keep accurate records of all your communications, including verbal.

- Take action on late payments, lodge all claims promptly; and lodge a charge or notice of claim for a debt or lien to gain priority in the event of insolvency.

If you’re a subcontractor or supplier:

- Get personal guarantees where credit is provided.

- Gain security over the company’s assets.

- Take advantage of your right to suspend work under the contract for non-payment.

- Include clauses in your contracts to protect ownership of materials and equipment.

- Register security interests on the PPSR so they are enforceable in the case of insolvency.

- Keep accurate records of all your communications, including verbal.

- Take action on late payments, lodge all claims promptly; and lodge a charge or notice of claim for a debt or lien to gain priority in the event of insolvency.

Additional actions to take

- Prior to entering into any contract, carry out ASIC director and related party searches on contractors to look for wind up documents, or company name changes – a sign of phoenix activity.

- Make sure bank guarantees for completed projects are returned in line with the contract.

- Carry out a PPSR search to identify the extent to which businesses are engaging new suppliers and not paying previous ones.

- Review your business structures/finances to identify security or guarantees provided to support loans, and how funds can be accessed if cash flow dries up.

- Properly and fully review any contract before entering the contract, including all general terms and the scope of works.

If despite your best efforts to curb the risk your building or construction business is facing financial difficulties, you need to act swiftly if you want to turn things around.

Chapter 2:

Turning your company around

First steps

- Thoroughly investigate your financial difficulties

- Keep accurate records and stay informed as to your company’s financial situation

- Seek help from a qualified advisor (e.g., an accountant) to determine your position

Engaging a turnaround expert

If you have concerns for the solvency of your company (see Chapter 4 page 13), you should swiftly engage a turnaround expert. They can help you identify problems and come up with a solution you may not have thought of. The sooner you seek help, the better your chances of survival.

Finding an experienced turnaround expert that understands your club is vital to the success of any turnaround strategy.

We’re always available for a free confidential consultation to talk through your turnaround options and how the process could work for your club – 1300 727 739 | enquiries@rgia.com.au

3 steps to turnaround

Step 1: Analysing the situation

Is your construction company in imminent danger of failure, do you have substantial losses but survival is not yet threatened, or are you simply in a declining business position?

For your business to be deemed viable, you must have:

- one or more viable core businesses

- adequate available financial resources, and

- sufficient organisational resources.

If these requirements are met, a detailed assessment of your strengths and weaknesses should be undertaken and stakeholder communication increased. If the above requirements are not met, go to 13 to consider other options for your business.

Step 2: Developing a strategic Turnaround plan

Your turnaround plan should have specific goals and detailed function areas. Management must also be accountable to deliver on these goals.

Step 3: Implementing the plan

If the review identifies that your company has any major financial issues, your turnaround plan must be implemented.

The seven key ingredients of a successful turnaround strategy are crisis stabilisation, new leadership, stakeholder focus, strategic focus, organisational change, critical process improvements and financial restructuring.

Your turnaround plan might involve:

- Determining your current labour requirements and making redundancies

- Changing your management team and structure

- Eliminating any unprofitable services your business offers

- Identifying any surplus assets (non-core assets) and determining if they can be realised in a timely manner

- Identifying assets that can be maximised for further value

- Eliminating any unnecessary capital expenditure or considering and prioritising capital expenditure that maximises return on investment

- Focusing on your cash flow

- Communicating with your employees, creditors and suppliers and financiers

Every situation is different, so will require different strategies. You might look at improving efficiencies and rationalising resources, such as negotiating temporary relaxed payment terms with creditors. Or you may need to downsize and make redundancies.

Importantly, these courses of action should be properly recorded. This includes having a written turnaround plan, a business review document, and advice prepared by an expert.

In the building and construction game, you may not have physical assets to sell to meet short term demands, so cash flow management is key. Once you start having cash flow issues, the knock-on effect can be reluctant subcontractors with inflated prices.

The ipso facto insolvency reforms, effective from July 1, 2018, prevent a party from exercising a right under a contract, agreement or arrangement that arises due to a formal insolvency restructuring including voluntary administration (VA), receivership or a scheme of arrangement. This includes a right to terminate your contract.

The best time to consider safe harbour is as soon as you suspect your company is approaching insolvency. The sooner you access it, the better protected you are.

Entering ‘Safe harbour’ – Avoiding insolvent trading liability

Under Section 588GA of the Corporations Act 2001 (the Act), if your company is taking actions to improve its financial situation (turnaround), you can access ‘safe harbour’.

Safe harbour is a form of legal protection that provides a defence from insolvent trading liability for directors (see Chapter 4). Importantly, safe harbour is only available where a genuine turnaround attempt is being made, and you meet the eligibility criteria referred to as the ‘better outcome test’.

To stay protected, you must be able to answer yes to the following questions:

- Are you informed about the financial position of the company?

- Are you taking appropriate steps to prevent misconduct?

- Are you taking appropriate steps to ensure your company is keeping proper financial records?

- Are you seeking advice from an appropriately qualified expert?

- Are you developing or implementing a plan for restructuring the company?

In addition to answering yes to all of these questions, you must also ensure your employee entitlements and superannuation are paid, and your ATO returns are lodged on time.

Case Study – Turnaround

“The key in any turnaround is to take action early. In this case, as in all cases, we worked with the business, its advisors, and its stakeholders to develop solutions in challenging and difficult situations with a positive end result.”

—MITCH GRIFFITHS (CO-FOUNDER / DIRECTOR)

Background

A large residential construction firm had been on an aggressive growth path leading up to an economic slowdown in the local area. Combined with headwinds and the existing market forces at play, this led to a cash flow crisis. We were called in to review the company’s situation and determine the most appropriate response to its circumstances.

Core problem

To avoid downsizing the business, the directors attempted to diversify and enter into a development agreement with landowners to share in the proceeds once the houses were sold. This tied up a significant proportion of the company’s working capital and was preventing it from starting new projects as a result of Home Owners Warranty (HOW) restrictions.

The solution

After assessing the business’ viability, we advised a business stabilisation/turnaround plan and that then triggered safe harbour protection. Our role in implementing the plan involved:

- Determining current labour requirements and making cuts where needed.

- Assisting with negotiations to exit the loss-making construction contracts.

- Identifying non-core assets and arranging a sale to pay down bank debt and assist the working capital shortfall.

- Negotiating a standstill agreement with the major financiers and assisting the CFO in negotiating a repayment plan for the ATO and other key suppliers.

- Recommending changes to the management team and structure.

- Eliminating unprofitable lines of business and unnecessary capital expenditure.

- Improving their accounts receivable collection process.

The outcome

As a result of accessing safe harbour and implementing the turnaround plan:

- The cash flow crisis was able to be managed appropriately.

- Stakeholder relationships were restored with confidence and integrity.

- The business was able to continue to trade and avoided a formal insolvency appointment.

- Creditors were repaid in full, and the majority of employees remained employed. Staff that were made redundant were paid in full, and shareholder value was preserved. The business’s economic value was stabilised.

- The business slowly returned to profitability. In addition, the strategic focus shifted from cashflow to profitability and return-on-equity, and on economic value-add.

We deal with many construction leaders, who are facing financial issues and insolvency. The solutions we deliver are highly-tailored to individual circumstances. If you feel your organisation could benefit from our assistance, we’re always available for a free, confidential consultation to talk through your options

– 1300 727 739 | enquiries@rgia.com.au

Small Business Restructing Plan (SBRP)

If you’re a small business experiencing financial difficulties, as of January 1 2021, you may be able to access the small business restructuring plan. This new formal turnaround option – part of the government’s COVID small business rescue reforms –offers an easier way to reduce debt and avert crisis, whilst remaining in control of your business.

SBRP process

The small business restructuring plan is a formal restructuring option; it’s a simplified, lower-cost formal appointment. The purpose of this new process is to support more small businesses to survive, meaning better outcomes for businesses, creditors, employees and the economy.

Eligibility criteria

To take advantage of this process, you must:

- be operated by a company;

- owe less than $1 million in liabilities (excluding liabilities to employees of the NFP);

- all outstanding employee entitlements, including superannuation, must have been paid (this does

- not include entitlements not yet due for payment, such as annual or long service leave);

- all tax lodgements for the company must be up to date.

- not have previously done a small business restructuring or used simplified liquidation in the past 7 year

Current and former directors (acting in the past 12 months) also cannot have been a director of a company that has done a small business restructuring or used simplified liquidation in the past 7 years.

How the SBRP process works

Step 1: Appointing a qualified small business restructuring practitioner (SBRP)

After announcing the decision to access restructuring, a qualified small business restructuring practitioner must be appointed. Their first job is to assess your situation and determine if your company is eligible to access the restructuring process.

Step 2: Drafting a small business restructuring plan

You and your practitioner have 20 days from the appointment to prepare a small business restructuring plan in the approved form.

The plan must:

- Identify the property that is being dealt with and how it will be dealt with (this could be via third party contribution, proceeds from the sale of assets, future trading profits or refinance)

- Provide remuneration for the SBRP appointment

- State the date on which it was executed

Once the plan is finalised you have five days to notify ASIC. Your practitioner must also prepare other relevant documentation, including a restructuring statement and a certification certificate.

Step 3: Serving of the business plan to creditors

Your practitioner must serve the plan and relevant papers to affected creditors. Note all employee entitlements must be paid and all tax reporting obligations up to date before this can happen.

Step 4: Acceptance or rejection of the plan

Once your creditors have received the plan, they have 15 days to vote on it via a written statement.

If disputed: A creditor must provide specifics of the dispute. Your practitioner then has five days to resolve it.

If the majority in value of creditors accept it: The plan will be approved, binding all unsecured creditors. It will then be administered as you continue to trade as normal.

If rejected: Your company may be placed into voluntary administration or simplified liquidation (see Chapter 5).

Rapsey Griffiths are experienced small business turnaround and restructuring practitioners. We can guide you through developing and administering a small business restructuring plan.

Contact us – 1300 727 739 | enquiries@rgia.com.au

Chapter 3:

Tackling insolvency

What is insolvency?

Insolvency is the state of being insolvent or unable to pay your debts as and when they are due and payable. If you’re facing it, it’s a daunting reality.

(1) A person (or company) is solvent if, and only if, the person (or company) is able to pay all the person’s debts as and when they become due and payable.”

(2) A person (or company) who is not solvent is insolvent —Section 95A of the Corporations Act 2001 (Cth) (the Act).

Warning signs of insolvency

Determining insolvency isn’t always easy. A forward-looking cash flow test can help you determine your company’s ability to pay its debts when they become payable. However, you also need to look at your wider financial position.

Insolvency checklist

- Continued losses over recurring financial reporting periods

- Inability to borrow money or obtain loan approvals

- Overdue taxes

- Poor liquidity ratios

- Inability to produce timely and accurate information on your company’s performance and financial position

- Dishonoured and post-dated cheques

- Special arrangements with certain creditors

- Sales of non-current assets (e.g., land, vehicles or equipment) to fund working capital deficiencies

- Inability to meet employee payment obligations (e.g., superannuation payments)

- Replacing standing creditor payment terms with discretionary decisions on when and which creditors will be paid

- Absence of any budget or basic financial plan/goals (e.g., seasonal periods may cause reductions in service hours/revenue and need to be planned for operationally to reduce expenses to prevent hours being spent on post-analysis of suspected revenue loss)

If your construction business is facing any of the above, you should take immediate action to turn things around (see Chapter 2).

It’s important to note the difference between a temporary lack of liquidity (you may still be solvent) and an endemic shortage of working capital.

Cash flow test

A cash flow test looks at whether your company can pay its liabilities, as and when they fall due. Because lengthy payment terms are typical in the construction industry due to the nature of big projects, these should be taken into account.

Balance sheet test

A balance sheet test involves looking at your balance sheet to work out whether your company would have more assets or liabilities if it were immediately wound up. In the construction industry, work-in-progress (WIP) is considered an asset.

If you don’t have the expertise to do these tests internally, consider seeking help from an external, independent expert.

Common causees of insolvency in construction

- Project lag – committing to a project when the economy is good only for the project to lag for another two years

- Cash flow issues – including late payment and bad debt

- Lack of profitability – the process of winning work is highly competitive and price sensitive. In many cases, the only way to win a contract is to charge the lowest price.

- Frequency with which suppliers and clients go out of business

- Availability and cost of credit

A successful turnaround with safe harbour protection (see Chapter 2) can steer you back to solvency and protect you from liability. But what are your legal obligations when it comes to insolvency?

Chapter 4

Understanding directors' duties

Who is a director?

The definition of ‘director’ under the Act includes shadow and de facto directors or any alternate director that is appointed and acts in that capacity.

Common law duties

Under common law, directors have a duty to:

- act in good faith and the best interests of the company;

- act with care and diligence;

- to avoid conflicts of interest; and

- to not improperly use company information.

If you allow your company to get into financial hot water or realise it’s insolvent or facing insolvency and fail to act, you’re failing to meet these duties.

The Corporations Act 2001 (the Act)

The common law duties are reinforced in the Corporations Act 2001 (the Act), which includes a duty to act with care and diligence (section 180 (2)) and in good faith, and a requirement for directors to not improperly use their position or information.

Keep your records in check

One of your specific duties under the Act is a duty to ensure that your business keeps adequate books and records. These must correctly record and explain your company’s financial position and performance and includes work-in-progress (WIP) reports.

Section 588G – Duty to prevent insolvent trading

Under Section 588G of the Act, directors have a duty to prevent insolvent trading. A person commits an offence if:

- they were director at the time the company incurred the debt; and

- the company was insolvent at that time or became insolvent by incurring a debt; and

- at that time there were reasonable grounds for suspecting the company was insolvent or would become insolvent.

Further provisions relating to insolvency are contained in Sections 588H-Z.

Available defences

As director, you have several defences open to you. These include reasonable grounds to expect solvency, reasonable reliance on information provided by others, absence from management (due to illness or other good reason), and reasonable steps to prevent incurring of debt(s).

However, these defences shouldn’t be relied on. Instead, you should take reasonable steps to identify the causes of your financial difficulties and take swift action prior to any breach occurring.

Consequences of breaches of duty

- Civil penalties of up to $200,000 (where there were reasonable grounds the director suspected insolvency and failed to act)

- Compensation proceedings for amounts lost

- Criminal charges of up to $220,000 or imprisonment for up to 5 years, or both (where the director suspected insolvency and failed to act)

- Disqualification from managing a corporation

Chapter 5:

When turnaround isn't an option

The two main formal insolvency appointments available to companies are voluntary administration and liquidation.

Voluntary administration

If your company is believed to be insolvent (or likely to become insolvent), you can appoint an independent administrator to take control. They will assess your businesses viability moving forward and undertake a range of other activities such as:

- Complying with statutory obligations (such as the ATO)

- Communicating with governments, authorities and employees

- Procuring funding

- Engaging external experts to review your internal controls and implementing measures to ensure its integrity

- There is a moratorium on creditors enforcing their claims during this period.

An administrator can also help you draw up a Deed of Company Arrangement (DOCA).

What is a DOCA?

A Deed of Company Arrangement (DOCA) is a binding arrangement between a company and its creditors governing how its affairs will be dealt with. It maximises the chances of a company continuing while providing a better return for creditors than winding up.(ASIC)

Your DOCA proposal may involve:

- A third party injecting cash into your business to partially repay creditor claims

- Your business contributing to a fund (managed by a deed administrator from trading profits) to partially repay creditor claims

When drawn up, your DOCA will be proposed and considered at a meeting of your company’s creditors. If your creditors accept it, you, as director, will generally resume control of your company.

The voluntary administration process typically takes 25 business days – enough time to get some clarity. However, the issues in a DOCA are generally not resolved in this timeframe.

Once the DOCA terms have been complied with, your company is released from administration and creditors can no longer recover any unpaid debts from prior to the administration.

Working through insolvency is a daunting task. We’re always available for a free, confidential consultation to talk you through the process and how it could work for your organisation – 1300 727 739 | enquiries@rgia.com.au

Case study – Voluntary administration & DOCA

“Using our expertise, we were able to simplify a complex problem and focused on the best outcome for the business. Working in collaboration with the business owners, their accountant and legal team, we achieved the best possible result for employees, creditors and shareholders.”

—CHAD RAPSEY (CO-FOUNDER / DIRECTOR)

Background

A small business group specialising in the repair, maintenance, and installation of automatic sprinkler and other fire protection systems for commercial premises got into financial difficulty after the first two years of trading. We were called in as voluntary administrators (VAs), taking control of their business and cash flow for two months.

Core problem

The group faced financial difficulty primarily due to aggressive unstructured growth (from $0-$2m in two years) without the right controls in place.

The directors had also received poor business advice. The result was approx $1.4m of ATO/OSR debt, difficulties in reconciliation, an unsecured debt position too high to trade out of, and no access to equity.

The solution

Working as voluntary administrators, we proposed the following solution:

- The implementation of a holistic business turnaround strategy alongside the newly appointed company accountant.

- An independent review into the business’s projected trade profitability and cash flow to verify viability.

- Formulation of a deed of company arrangement (DOCA) between the company and creditors to satisfy the business’s existing debts.

The outcome

The creditors accepted the proposal set out in the DOCA. This led to them receiving greater returns than liquidation. Additional benefits of the acceptance of the DOCA included:

- Monthly monitoring and compliance reporting assistance to ensure continued viability

- Maintenance of all further tax and employee obligations

- Avoidance of complexities associated with the group structure

- Avoidance of a court application to appoint a receiver over the trust business assets

- Estimated intra-group and related party claims removed from the creditor pool

- Employees job retention avoiding their crystallisation of employee entitlements and redundancies

- Employees received 100% of their employee entitlements

- Unsecured creditors received a return of 19c /$

- The company’s debts were reduced by approximately $1.134 million

As a result of completing this voluntary administration turnaround alongside the new accountant and directors, the group is continuing to trade profitably.

Liquidation

Liquidation is usually considered as a last resort but offers a more conclusive outcome. It’s a formal appointment that terminally winds up the affairs of your company if you can’t pay your debts when they are due. This is generally a shutdown scenario.

The winding up process

During liquidation, control is handed to the liquidator. The process involves selling off your company’s assets, winding up your company’s financial affairs, breaking up the company structure, then figuring out what happened. In addition, bank accounts are frozen and employment terminated.

Key considerations

In a formal insolvency appointment, the administrator or liquidator will consider the following industry-specific issues, including the impact on contracts, bank guarantees, set-off, home warranty (residential), insurances and environmental and WHS.

How do I pay laid off employees?

If there’s not enough money to pay employees their entitlements in a liquidation scenario, these are covered by the Fair Entitlements Guarantee. Entitlements include unpaid wages, annual leave, long service leave, and redundancy pay.

Public reputation

As formal insolvency appointments are typically made public, you may be concerned about the negative impact this will have on your business, e.g., contract terminations. However, by avoiding a formal insolvency appointment, you can make the situation worse, including breaching your obligations under the Act.

In many cases of liquidation or voluntary administration, an organisation can be sold or merged with another organisation, preventing redundancies.

Case study – Voluntary liquidation

“Clarity makes resolution easier to achieve. By working together, we can put mechanisms and processes in place that help move things towards a suitable outcome.”

— MITCH GRIFFITHS (CO-FOUNDER / DIRECTOR)

Background

A medium-sized construction company specialising in residential property found itself in financial difficulty due to a range of internal and external factors, including defective work claims. We were called in to review the company’s particulars and identify the most appropriate response to its challenges.

Core problem

Following a business viability review, we determined the company was insolvent and unable to continue trading. As the owners and managers were experiencing high levels of stress and the business was lacking the capacity to undertake a turnaround strategy, we needed to provide a way for the company, its stakeholders and its creditors to move forward.

The solution

Given the company’s inability to pay its significant debts as and when they fell due, we determined the best solution would involve:

- Entering creditors’ voluntary liquidation (also known as business liquidation)

- Establishing and realising the assets of the company

- Communicating with employees and creditors regarding the liquidation process

- The liquidator dealing with incomplete construction projects and assisting customer claims under the home building compensation scheme

The outcome

While liquidation is generally a last resort, the benefits of undertaking the creditors’ voluntary liquidation reduced the risk of insolvent trading and ended the defective work claims. It also:

- Averted a standard director penalty notice (DPN) being issued by the ATO (subject to lodgements being made on time)

- Enabled employment entitlements to be paid in full via the Fair Entitlements Guarantee (FEG) scheme

- Saw employee superannuation paid from the assets realised by the liquidator

- Allowed customers to have their projects completed by another construction company

- Resulted in unsecured creditors receiving a distribution of 10c /$

- Releasing the company from debts of approximately $840,000.

The liquidation helped the directors to comply with their duties, providing employees and creditors with a return on outstanding debts.

We deal with many construction leaders who are facing financial issues and insolvency. The solutions we deliver are highly-tailored to individual circumstances. If you feel your company could benefit from our assistance, we’re always available for a free, confidential consultation to talk through your options – 1300 727 739 | enquiries@rgia.com.au

Additional Resources

Insolvent Trading | Australian Institute of Company Directors

Building & Construction Industry Fact Sheet | GOV

Types of building and construction businesses | ATO

PPSR | Australian Financial Security Authority

Online Business Insolvency Assessment

Corporate turnaround: What you need to know National Disability Insurance Scheme | NDIS